Chapter 8: Credit

APR represents the cost of borrowing on a yearly basis, including interest and fees. Credit card APRs can vary based on your creditworthiness and the type of card, although they typically average 20-30% (which is insanely high). It’s important to understand the difference between the purchase APR, cash advance APR, and penalty APR. Always aim to pay off your full balance each month to avoid interest charges entirely.

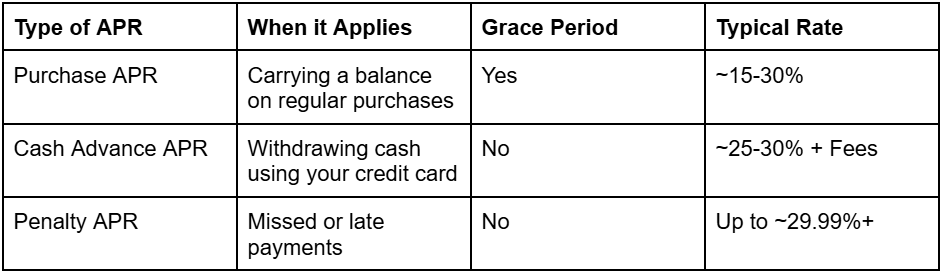

Purchase APR

What it is: The Purchase APR is the interest rate charged when you carry a balance on regular purchases made with your credit card.

When it applies: If you don’t pay your full statement balance by the due date, interest will begin to accrue on the remaining amount at the purchase APR.

Important Note: Many credit cards offer a grace period, typically around 21–25 days, during which you can pay your balance in full and avoid interest altogether.

Cash Advance APR

What it is: This is the interest rate charged when you withdraw cash using your credit card—either from an ATM or through a convenience check provided by the card issuer.

When it applies: Interest starts accruing immediately, with no grace period. This means you’ll start paying interest from the day you take out the cash advance.

Why it matters: The cash advance APR is usually much higher than the purchase APR, often exceeding 25% or more. Additionally, cash advances often include a transaction fee (e.g., 3-5% of the amount withdrawn).

Penalty APR

What it is: This is a much higher interest rate that may be applied if you miss a payment or make a late payment.

When it applies: If you violate the terms of your credit agreement—especially by paying late—the issuer may trigger the penalty APR.

How high it can go: Penalty APRs can be as high as 29.99% or more. Once applied, it may stay in effect for months or even indefinitely, depending on the issuer’s policy.

How to avoid it: Always pay at least the minimum payment on time to avoid triggering this costly rate.