Chapter 3: Entity Types

An S Corp is a type of tax designation for an LLC. LLC’s are typically taxed as pass-through entities, meaning the profit or losses of the LLC are passed onto the members based on their percentage ownership (more on this later). This is convenient come tax season, but it also means that you’re personally liable to pay self employment tax on 100% of your share of the LLC’s profits. Self employment tax (FICA) is 15.3% on the first $168,600 of personal income you have in a given year (as of 2024), and covers Medicare and Social Security taxes. For someone with a normal job, your employer will pay 50% of this tax, so a person working a W-2 job will only pay ~7.65% tax for Social Security and Medicare.

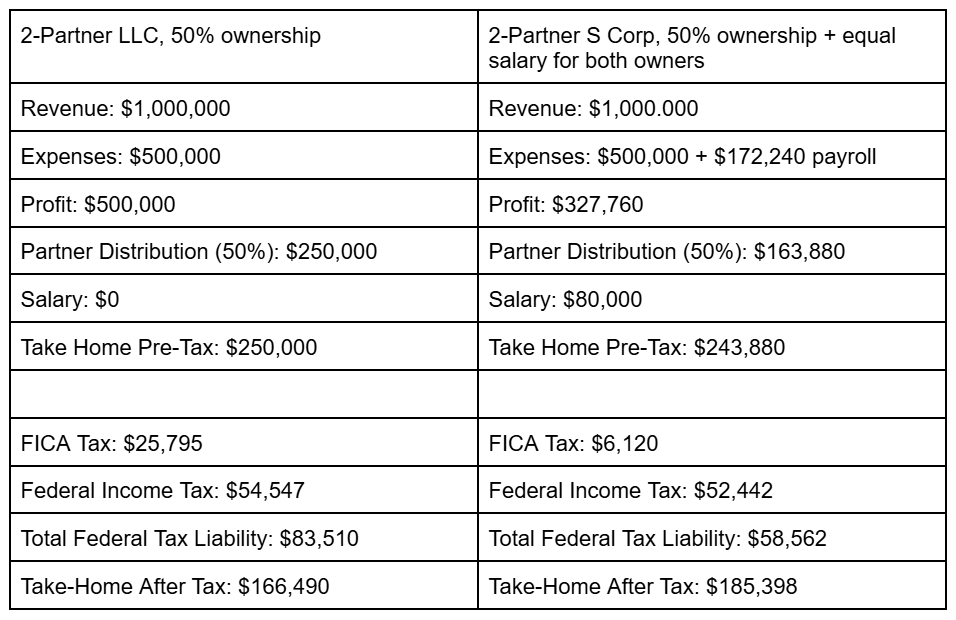

An LLC can apply to become an S Corp within the first 75 days of each calendar year. Becoming an S Corp allows an owner to become a W-2 employee for the company he owns, and pay himself a “reasonable” salary. By paying yourself a salary, the company is responsible for 50% of the aforementioned self employment tax (FICA), thus reducing your personal tax burden and allowing the company to deduct its share of the self employment tax (or “payroll tax”) as a business expense. The main benefit however is in the distributions: whatever you don’t pay in salary, you can distribute as profit, and these distributions are NOT subject to the self employment tax. This can be tricky to understand, so take a look at the example below:

The numbers can get a bit weird, but notice how much the personal FICA liability drops! Your take home pay after taxes is actually $19,000 more by paying yourself a salary as an S Corp, even though your pre-tax earnings are nearly $7,000 less. Your company is taking some of the burden off your shoulder and deducting the taxes as a business expense, while you collect distributions only subject to federal income tax. This practice scales up amazingly, with increased savings the more money your company makes (and therefore the larger salary you can reasonably take). You can mess around with different salary numbers to see how it affects your bottom line, but in general, it’s better if you can load as much of your FICA tax burden on your company as possible and maximize your distributions.